No spam - just the latest insights!

Join over 30,000 industry professionals who subscribe for free

Subscribe for free!

We'll never share your information or send you spam

Ryutaro Kawamura has broad experiences in international investments, especially on cross-border shipping, infrastructure and real estate development projects in Southeast Asia, and financing for those projects. He has been actively involved in the projects in Singapore, Malaysia, Indonesia, India, Vietnam, Thailand, and Philippines. Such projects include shipping finance, utilising his work experience in international shipping transactions and dispute resolutions. For recent years, he has led the maritime practice of the firm as the Head of the practice group.

Yusuke Nakajima has extensive experience in asset financing transactions and real estate financing transactions, and co-leads the asset financing team at Mori Hamada & Matsumoto.

He has considerable experience in a wide range of asset financing work, including ship and aircraft JOLs and JOLCOs. He also has considerable experience in a wide range of real estate work, including logistics, accommodation, residential and other commercial properties. He advises both international and domestic financial institutions, leasing companies, commercial companies and investors on all aspects of asset financing transactions, including acquisitions, disposals, leasing and financing transactions. He also covers regulations applicable to asset financing transactions and real estate transactions including structuring funds for investment.

In this chapter, we will introduce the “Japan Operating Lease with Call Option” (“JOLCO”), which is a unique financing structure in Japan used for ship financing. We will also provide an overview of the reform of the maritime law in 2018.

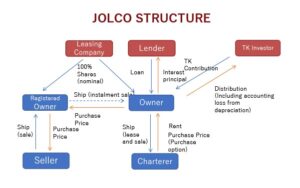

A JOLCO is a structure adopted for ship financing transactions arranged by Japanese leasing companies. This structure is also used for financing transactions for aircraft, containers, and other valuable equipment.

(1) Outline of the structure

(i) Origination In a JOLCO transaction, a special purpose company (the “Registered Owner”) incorporated in a foreign jurisdiction (usually the jurisdiction where the ship is registered), which is usually a wholly-owned subsidiary of a leasing company, purchases a ship with the funds received from the SPC and registers it in the relevant jurisdiction. Another special purpose company (the “SPC”) incorporated in Japan, which is also usually a wholly-owned subsidiary of a leasing company, purchases a ship with funds financed by way of (i) a non-recourse loan from third party lenders, secured by the ship and (ii) a “tokumei kumiai” (“TK”) investment from equity investors (the “Investors”), as more fully described below. In order for the Registered Owner to maintain legal title to the ship for the registration, the purchase price is paid on an instalment basis. The SPC pays a substantial portion of the purchase price at the beginning, and a

nominal residual amount will be paid in the future. Although the amount of capital contribution by the leasing company is nominal, the leasing company as a parent having control over the Registered Owner and the SPC is often required to provide a comfort letter or keep-well letter (called “parent undertaking”) in favour of the lenders or charterer, as the case may be. In the context of structured financing transactions involving special purpose companies in Japan, lenders often require that the special purpose companies be an orphan entity (for bankruptcy remoteness). However, in a JOLCO transaction, it is usually not required in practice.

(ii) Charter Period During the charter period, the SPC bareboat-charters the ship to a shipping company (the “Charterer”) and receives charterhires from the Charterer. The charterhires from the Charterer are first applied to payments of interest and/or principal of the non-recourse loan, and the remaining rents charterhires are distributed to the Investors.

(iii) Purchase of Ship by Charterer Under the bareboat charter agreement, the Charterer is given an option to purchase (call-option) the ship at a certain price, exercisable after a certain period from the commencement of the charter. In practice, it is usually anticipated that the Charterer will exercise this option and purchase the ship. However, since, legally speaking, this is an option for the Chatterer, it is not guaranteed that the Charterer will purchase the ship. If the ship is purchased by the Charterer, the proceeds from the sale are first applied to payments of the outstanding amounts in respect of the loan and the remaining proceeds are distributed to the Investors.

Below is a sample chart of a typical JOLCO structure.

(2) Relevant Japanese Laws

In JOLCO transactions, the main areas where Japanese laws are involved are as follows:

The following matters/documents are governed by Japanese law:

– Incorporation and governance of the SPC (i.e., the Companies Act of Japan);

– Certain security agreements to be entered into to create a security interest in favor of the lenders e.g. share pledge agreement (SPC’s share) and account pledge agreement (when the bank is a Japanese bank); and

– TK agreements with the Investors. Other transaction documents (e.g. a purchase and sale agreement, instalment sale agreement, bareboat charterparty agreement, loan agreement, and security assignment of certain contractual rights) are usually governed by English law or New York law. The mortgage agreement is governed by the law of the jurisdiction where the ship is registered (e.g. Panama, Liberia, Marshall etc.).

– Financial Instruments and Exchange Act of Japan (the “FIEA”): Since the TK Investment (defined below) constitutes a “security” (yuka-shoken) under the FIEA, a leasing company usually has a Type II Financial Instruments Business License, which enables the leasing company to solicit investors to purchase the TK investment. Please also see section 3.(3) below for more details.

(1) TK Investment

(a) Nature of TK Investment

In JOLCO transactions, the investors make contributions to the SPC by way of a Japanese anonymous or “silent” partnership (tokumei kumiai) investment under the Commercial Code of Japan (“TK Investment”). The TK Investment has the following nature:

– A TK investor executes a TK agreement with the SPC. A TK agreement is a two-party agreement between an operator and an investor. Thus, if there are multiple Investors, the SPC enters into a TK agreement with each Investor, resulting in a number of TK agreements executed by the SPC. A TK investor makes a capital contribution to the SPC pursuant to the TK agreement, and the SPC as a TK operator will carry out the TK business (i.e. purchase, charter and sale of a ship).

– A TK investor has no voting right or any right to be proactively involved in the management of the TK business. Simply said, a TK investor is a “passive” investor.

– A TK agreement does not establish any distinct legal entity. All rights and obligations of the TK business to third parties solely vest in the TK operator, and the TK investor never has any right, or incurs any obligation, directly to third parties. The TK investor is effectively behind the TK operator in relation to those third parties.

– In JOLCO transactions, since a TK investor never has a direct relationship with a third party, the TK investor does not usually appear in the operative documents vis-à-vis the TK business. As such, the TK business is conducted by the SPC as if the SPC were acting on its own behalf.

– The net profit and loss of the TK business are allocated to the TK investor for accounting and tax purposes (i.e., pass-through treatment). In other words, Japanese corporate tax is not imposed on the profit of the TK business at the level of the TK operator (the SPC).

– A TK investor is also entitled to a cash distribution from the net profit (if any) of the TK business from the TK operator but return of principal is not guaranteed. Since the distribution is made from net profit (after paying other claims, loan etc.), a TK Investment is different from loans or bonds, which constitute definitive rights for repayment of agreed-upon amounts. A TK Investment is more akin to equity (at least in an economic sense), although once the concrete claims for distribution accrue pursuant to a TK agreement, the TK investor has the same priority as other claimants just like claims for distribution with respect to stocks or trust beneficial interests.

– Although the accounting loss is allocated to a TK investor, the TK investor is not required to make additional contributions to the TK business unless otherwise agreed in the TK agreement.

– In general, a TK investor is like a limited partner and its risk is, at maximum, the amount of the principal which it contributed. Please note, however, that in JOLCO transactions, it is sometimes agreed that the TK investor must make additional contribution to the TK Operator up to a certain amount in the event of shortfall in the TK business.

– In JOLCO structures, a majority of the TK investors are ordinary business companies (not institutional investors), including family offices in Japan.

(b) Tax Benefit for TK Investors

The most unique features of JOLCO transactions are the tax benefits for TK investors. Just like other asset financing transactions, TK investors can enjoy (i) distribution of profits made out of charterhires payable by the charterer during the charter period, and (ii) proceeds from the sale of the ship at the end of the lease period.

In addition, the accounting loss from the depreciation of ship is allocated to the investors in JOLCO transactions. A ship can generally be depreciated faster than other assets and, during the first couple of years of the lease, the accounting loss from the depreciation is larger than the profit from charterhire payments. As a result, the investor can off-set that loss against profits from its ordinary business other than the ship leasing business and consequently defer its tax payment. Furthermore, as the economic life of a ship is longer than the depreciation period, the investors may be able to recoup additional value when they exit the investment (i.e. sale of the ship).

(2) Form of SPC

In JOLCO transactions, an SPC is used from commercial points of view to own and hold a ship (although the legal owner of the ship is the Registered Owners). If a leasing company relies on the exemption with respect to an underwriting business under the FIEA (for more details, see sub-section (3) below), the SPC must be a stock limited liability company, which is a kabushiki kaisha (“KK”) (including a Japanese Tokurei Yugen Kaisha (special limited company) under the Companies Act), under the Companies Act of Japan.

In practice, KK is most commonly used in JOLCO transactions.

A KK has shareholders and directors. Usually, directors are dispatched from the leasing company. The directors operate the company’s business and are generally responsible for executing any contract which the company is to become a party to. Internal authorisation is made by the directors’ decision or shareholders’ approval at a shareholders meeting, as the case may be.

(3) Financial Instruments and Exchange Act

A leasing company originates a transaction and solicits equity investors to invest in a ship leasing business in the form of a TK. TK Investments are included in the list of securities defined under Article 2, paragraph 2 of the FIEA (“Type II Securities”). A person who engages in the sale and purchase of Type II Securities is required to have a “Type II Financial Instruments Business” license under the FIEA.

Apart from the foregoing, a “Type I Financial Instruments Business” license under the FIEA is required to conduct an “underwriting” business even if the underwritten securities are Type II Securities. A Type I Financial Instruments Business license is subject to more stringent regulations than those applicable to the Type II Financial Instruments Business license. However, there is an exemption specifically tailored for equipment leasing transactions. If (i) a person who intends to underwrite TK Investments has a Type II Financial Instruments Business license, (ii) that person is a 100% parent company of the TK operator which is a KK, (iii) the TK operator conducts its equipment leasing business as the TK business, and (iv) certain other conditions are met, that person will not be required to obtain a Type I Financial Instruments Business license in order to underwrite the TK Investments.

In Japan, the major source of maritime law is Part III of the Commercial Code (Maritime Commerce). This part has rarely had substantial reform since the Commercial Code was enacted in 1889. In 2018, in response to the changes in social and economic conditions following the enactment of the Commercial Code, Part III of the Commercial Code was revised alongside the Act on the International Carriage of Goods by Sea to modernise the rules of transportation and maritime commerce.

Although the reform is quite extensive, in terms of the ship financing, the reorganisation of the maritime liens is the most important.

Under the revised Commercial Code (Article 842), a creditor who has any of the following claims is entitled to maritime liens:

(i) a claim to compensation for loss or damage due to harm to an individual’s life or person that has arisen in direct connection with the operation of the ship;

(ii) a claim for the salvage charges or a claim based on the contribution of a general average to be borne by the ship;

(iii) a claim that can be collected pursuant to the National Tax Collection or using procedures for collecting national taxes and that arises in connection with the ship’s entry into a port or use of a port or in connection with other navigation of the ship; or a claim for pilotage charges or towage charges;

(iv) a claim for costs necessary for continuing a voyage; and

(v) a claim held by the master or other officer/crew arising from an employment contract. Under the Japanese law, in addition to the maritime liens under the revised Commercial Code above, maritime liens are granted to the holders of a claim subject to limitation under the Act on Limitation of Shipowner Liability and the Act on Liability for Oil Pollution Damage.